Washington’s recent budget deal represents at best a tiny baby step in the right direction. What is at stake in the budget battles to come is exponentially higher. This is why the “Maxed Out America” initiative of the PJ Institute demands the immediate attention of the political class and the American people.

Everyone knows that an individual or family can only afford to go so far into debt before they become “maxed out.” At that point, lenders charge higher interest rates, refuse to extend additional credit, and cut existing credit lines.

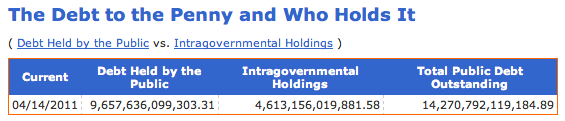

The idea that there are limits on borrowing applies equally to the federal government, but its determination and ability to avoid grim reality have been much greater. For decades, Beltway politicians, with recent assistance from the Federal Reserve, have used tools not available to individuals and families to push off the government’s reckoning date. As of April 14, they have run up the nation’s “debt held by the public” — really amounts owed to individuals, corporations, and other countries — to over $9.6 trillion, an amount that is roughly 65% of the nation’s annual output, or Gross Domestic Product (GDP).

{kind=link}

How far can a government run up its debts before lenders either decide to stop lending or raise their interest rates? As PJ Institute economist Laurence Kotlikoff noted in an early April column, there is a consensus that a country reaches “a critical insolvency threshold” once its public debt hits 90% of GDP. At that point, lender cutoffs and interest-rate premiums become real possibilities. Call it the point where we become “Maxed Out America.”

How far are we from the 90% Maxed Out America threshold? Not far at all.

Kotlikoff notes that the “alternative fiscal scenario” released by the Congressional Budget Office (CBO) in June 2010 “had us going critical … in 2021.”

Since then, a lot has happened. Unfortunately, almost all of it has brought Maxed Out America closer:

– In December, Congress and the president agreed to keep the current income tax system in place through the end of 2012, and to cut individual Social Security taxes by two percentage points during 2011. Kotlikoff calculates that these actions alone moved us two years closer to Maxed Out America.

– Kotlikoff further notes that CBO’s March 18 forecast which incorporated the president’s budget assumed that income tax rates will remain essentially unchanged for the next ten years.

That moved Maxed Out America to late 2017, a scant 6-1/2 years from now.

Since the recession began, CBO’s estimates of federal tax collections have been consistently overoptimistic. For example, it originally thought that fiscal 2010 collections would come in at $2.268 trillion. Actual collections were over $100 billion lower. CBO estimates that collections will grow by 14% in fiscal 2012 and 2013, and by another 11% in fiscal 2014, reaching over $3.2 trillion. With the economic recovery remaining sluggish at best, there’s reason to doubt that these increases will materialize.

{kind=link}

– Further complicating matters, lackluster employment growth since the recession ended in June 2009 has been dominated by temporary employees. Temp services have added 508,000 workers in the seven quarters since the recession ended, while the rest of the economy has lost — that’s right, lost — 263,000 jobs. Temps are usually paid less than full-time employees, and therefore generate less in payroll and income tax collections for Uncle Sam. If this trend continues, actual collections will lag CBO’s estimates even further.If we’re lucky, the positive results of the recent 2011 budget deal might offset the negative effect of the last two factors just cited, and we still have 6-1/2 years until Maxed Out America arrives.

{kind=link}

At least one influential entity is concerned that we may have nowhere near that much time. Last Monday, ratings agency Standard and Poor’s cut its long-term outlook on U.S. sovereign debt for the first time from “stable” to “negative.” The firm believes that there is a one-third chance that it will have to issue an actual downgrade of our debt in the next two years. If ratings agencies and lenders determine that we are not serious about addressing our problems, they may begin to raise rates or reduce their exposure even before we hit the Maxed Out level.

The real problem, of course, is spending, which, even after the budget deal, will have grown by over $1 trillion in four years, or about 40%, by the end of fiscal 2011. Maxed Out America cannot be avoided at currently projected spending levels.

The PJ Institute’s Maxed Out America Special Report has a stern warning about the consequences of doing nothing: “Our sixteen year old kids, entering the tenth grade of high school in the fall, may face this economic impact when they graduate from college in 2017, if not sooner.” Are we as a nation willing to accept that possibility?

Given the oncoming calamity, Washington’s lack of serious urgency is scandalous. The Maxed Out America initiative intends to change that. Readers should ensure that their congressperson and senators understand that they, and we, are quickly running out of time.

No comments:

Post a Comment